Retirement Preparation with Milan Schwarzkopf | TGD

Retirement preparation is the process of aligning income, benefits timing, health-care reserves, daily purpose, and relationships before leaving work so your next chapter is financially sustainable, personally meaningful, and resilient against inflation, market swings, and longer lifespans.

Retirement preparation is the process of aligning income, benefits timing, health-care reserves, daily purpose, and relationships before leaving work so your next chapter is financially sustainable, personally meaningful, and resilient against inflation, market swings, and longer lifespans.

Key Takeaways

- Retirement can last 20-30 years or more, so the plan must cover income, health, and daily structure across decades.

- According to the Social Security Administration, claiming can start at 62 and monthly benefits rise through age 70, so timing changes the income picture.

- According to Fidelity Investments, a 65-year-old retiring in 2025 may spend $172,500 on health care during retirement.

- This TGD course is intermediate and coaching-based, which makes it useful for people who want a personalized roadmap.

- The course connects money, purpose, health, relationships, and legacy instead of treating retirement as a single financial decision.

Table of Contents

- Understanding Retirement Preparation

- Retirement Planning Concepts and Techniques

- Who Benefits from Learning Retirement Preparation?

- What Do Students Say?

- Is This Course Worth It?

- About the Creator

- Retirement Planning Essentials

- Watch Before You Enroll

- Frequently Asked Questions

- Conclusion

- Explore More on TGD

Understanding Retirement Preparation

Retirement preparation is about making the transition from earning to living sustainable. It combines income planning, benefit timing, health care budgeting, and lifestyle design so the next 20 to 30 years do not depend on guesswork. According to the Internal Revenue Service, 2026 employee elective deferrals can reach $24,500 for 401(k), 403(b), governmental 457, and Thrift Savings Plan accounts, while traditional and Roth IRAs are capped at $7,500. That shows there is still room to act late in a career.

Social Security is another moving piece. According to the Social Security Administration, benefits can start between ages 62 and 70, and waiting longer raises the monthly amount. The agency also says 2026 beneficiaries will receive a 2.8% COLA, which helps but does not erase inflation risk. Fidelity Investments estimates a 65-year-old retiring in 2025 may spend $172,500 on health care during retirement. EBRI / Greenwald Research found 81% of workers worry rising living costs will make it harder to save as much as they want.

Want to Learn Retirement Preparation Step by Step?

This course on The Great Discovery covers these fundamentals in a more structured format, with a personalized and done-with-you approach.

The Great Discovery (TGD) is a global online course marketplace where creators publish courses and learners discover practical training across business, technology, wellness, and personal growth.

Retirement Planning Concepts and Techniques

Retirement works best when you treat it as a system, not a single decision. The most useful plans connect money, health, purpose, and relationships so the transition feels deliberate instead of reactive.

Map Your Income Stack

Most retirement plans start by listing every income source you will rely on. That includes Social Security, workplace plans, IRAs, taxable savings, pensions, and any part-time work you expect to keep. The point is not only to know how much you have, but also to know when each stream starts, how stable it is, and what tradeoffs come with drawing it early or late.

Choose a Social Security Strategy

According to the Social Security Administration, you can claim benefits as early as 62 or delay until 70. Waiting longer usually raises the monthly benefit, so the decision should be based on health, household cash flow, and whether a spouse depends on your benefit record. A strong plan tests a few claiming ages before settling on one.

Plan for Health Care as a Core Expense

Health care often becomes one of the largest retirement costs, which is why it belongs in the first draft of the plan, not the last. Fidelity Investments estimates a 65-year-old retiring in 2025 may spend $172,500 on health care and medical expenses throughout retirement. That means premiums, deductibles, prescriptions, and out-of-pocket costs all need room in the budget.

Build an Inflation Buffer

Inflation turns small gaps into large ones over time. EBRI / Greenwald Research found that 81% of workers worry rising living costs will make it harder to save as much as they want, which is why retirement budgets need flexibility. A good buffer can include lower fixed costs, a cash reserve, and annual spending reviews.

Design Purpose, Routine, and Support

Retirement is also a life-design problem. You need a weekly rhythm, relationships that still feel alive, and a sense of contribution that does not depend on your job title. The best retirement plans treat purpose and legacy as practical planning items, not soft extras.

Who Benefits from Learning Retirement Preparation?

This topic helps anyone who wants a retirement plan that covers money, meaning, and daily life. The course sits in Coaching, Retirement, TGD Success, and Life Balance, so it is aimed at people who want structure and practical follow-through.

Ambitious Professionals in Their 40s, 50s, and 60s

If retirement is approaching but still feels abstract, this is the time to get specific. A personalized, done-with-you course is especially useful for people who want help turning broad goals into a real action plan. Because the course is intermediate, it fits readers who already understand the basics and want guidance on applying them.

People Who Want a Roadmap, Not a Generic Checklist

Some learners do not need more theory; they need a sequence of decisions. This topic matters if you want to connect savings, Social Security, health care, and lifestyle into one coherent plan. The coaching format can help when you want accountability as much as information.

Couples and Households Making Joint Decisions

Retirement affects a household, not just one person. Benefit timing, medical costs, housing decisions, and daily routines all land differently when two people are involved. A structured retirement process helps couples coordinate instead of guessing separately.

People Who Care About Purpose and Legacy

If you think retirement should be a new chapter, not an empty stop, this course fits that mindset. The description emphasizes health, wealth, happiness, fulfillment, and legacy, which makes it a strong starting point for readers who want retirement to feel intentional. That is where TGD's life-balance angle becomes useful.

What Do Students Say?

This course is new to the marketplace and hasn't collected reviews yet. Check back after launch for student feedback. For now, the best signals are the creator bio, the intermediate skill level, and the clarity of the course promise.

Is This Course Worth It?

Yes, if you want a structured retirement roadmap. It is best for people who want help connecting money, purpose, health, and relationships into one practical plan. The coaching format and intermediate level suggest it is built for learners who want applied guidance rather than surface-level advice.

It is not the best fit if you only want a narrow technical deep dive into tax law, legal setup, or a one-off calculator. It is also less useful if you already have a detailed retirement team and only need isolated facts.

The strongest reason to choose it on TGD is the combination of personalization, done-with-you structure, and a topic that benefits from customization. If you want a tailored 3-month action plan instead of generic retirement advice, this is a practical next step.

About the Creator

Milan Schwarzkopf Interactive Seller s.r.o. is the creator behind this retirement course. Public catalog data shows 4 courses created, 0 total learners, and an average rating of 0.0. The bio describes the creator as a Purposeful Retirement Expert and author.

That positioning matches a course built around retirement readiness, life balance, and long-term planning. If you want to see the creator directly, visit the profile here: https://thegreatdiscovery.com/creators/creator/mila-s?affiliate=account

Retirement Planning Essentials

Retirement planning becomes easier when you break it into a few repeatable decisions. This table turns a broad topic into a practical reference you can use while you plan.

| Planning Area | What It Covers | Why It Matters |

|---|---|---|

| Income stack | Social Security, workplace plans, IRAs, taxable savings, pensions, part-time work | Shows how money will arrive and whether it is stable enough to support long retirement years |

| Claiming age | When to start Social Security, from 62 to 70 | Changes the size of the monthly benefit and the timing of cash flow |

| Health care reserve | Premiums, deductibles, prescriptions, and out-of-pocket medical costs | Prevents medical spending from crowding out basic living expenses |

| Inflation protection | Flexible spending, emergency cash, and periodic budget reviews | Helps the plan survive higher prices over 20 to 30 years |

| Purpose and routine | Weekly structure, relationships, volunteering, learning, and contribution | Makes retirement feel like a meaningful chapter instead of an aimless gap |

| Legacy planning | Family priorities, support systems, and long-term wishes | Keeps the retirement conversation focused on values, not just balances |

These building blocks explain why a strong retirement course should cover more than savings alone. The course's personalized structure is useful if you want help turning these concepts into a plan you can actually follow.

Master Retirement Preparation with Expert Guidance

Milan Schwarzkopf Interactive Seller s.r.o.'s course covers the same planning areas you just saw in the table, with a personalized and done-with-you format. It is built for readers who want structure, accountability, and a practical roadmap.

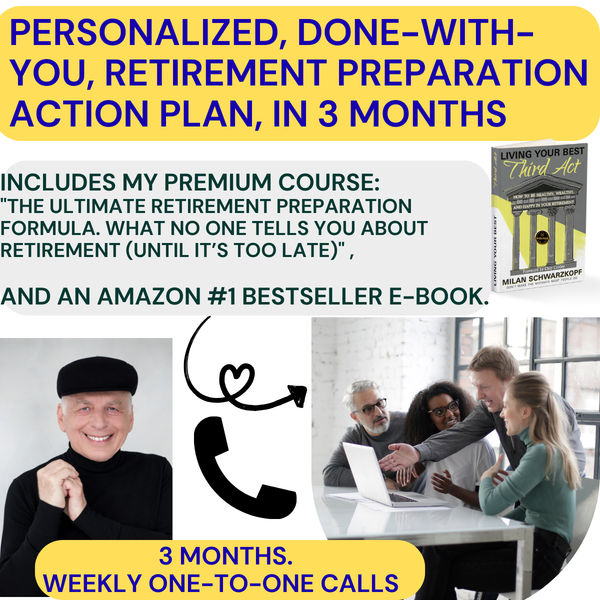

Enroll in Personalized, done-with-you, Retirement preparation action plan, in 3 months →

Watch Before You Enroll

If you want to understand TGD affiliate sharing, this walkthrough is the right primer. It explains the platform flow before you start posting links or recommendations.

Learn how to become an affiliate on The Great Discovery — the best affiliate program for course creators and marketers in 2026. Start earning commissions by sharing courses you believe in.

Frequently Asked Questions

These are the most common retirement questions people ask before they plan a next step. The answers below focus on the topic itself, with one question at the end about the TGD course.

What is retirement preparation?

Retirement preparation is the work of aligning income, benefits, health care, routine, and relationships before you stop full-time work. It matters because retirement can last 20-30 years or more, so the transition needs more than a savings account.

When should I start retirement planning?

Start as early as you can, because contribution limits, benefit timing, and habit changes work better over time. According to the Internal Revenue Service, 2026 401(k) elective deferrals can reach $24,500, which shows how much room some late-career savers still have.

How does Social Security affect retirement income?

According to the Social Security Administration, benefits can begin at 62 and rise the longer you wait, up to age 70. That means the best claiming age depends on your health, household income, and whether you need more cash flow now or a larger monthly benefit later.

How much should I budget for health care in retirement?

Health care is a major retirement expense, not a side note. Fidelity Investments estimates a 65-year-old retiring in 2025 may spend $172,500 on health care and medical expenses throughout retirement.

What are the biggest retirement planning blind spots?

The biggest blind spots are inflation, health care, and purpose. EBRI / Greenwald Research found that 81% of workers worry rising living costs will make it harder to save as much as they want, which is why flexible budgeting matters.

Who is this TGD course best for?

The course is best for intermediate learners who want a personalized, done-with-you retirement plan. Its coaching and life-balance framing suit people who want guidance that connects finances with purpose and daily structure.

Ready to Go Deeper?

You have learned the fundamentals of retirement preparation, including income timing, Social Security, health care, inflation, and the life changes that shape the transition. This course turns those ideas into a personalized plan.

Start Learning Retirement preparation on TGD →

Conclusion

Retirement preparation is a full-life planning task, not just an investing task. The big decisions are straightforward: know your income sources, understand Social Security timing, budget for health care, build protection against inflation, and design routines that give retirement purpose. If you want help turning those ideas into a personalized plan, the course is the next logical step on TGD: Explore the course on The Great Discovery.

Explore More on TGD

These links help you keep exploring retirement-related and adjacent TGD categories. Because there are no related courses in the current data, category pages are the cleanest fallback.

- Coaching courses on TGD

- Retirement courses on TGD

- TGD Success courses on TGD

- Life Balance courses on TGD

- Creator page for Milan Schwarzkopf Interactive Seller s.r.o.

- The Great Discovery homepage

Share Your Knowledge on The Great Discovery

Join Milan Schwarzkopf Interactive Seller s.r.o. and hundreds of other creators sharing their expertise. Create and sell your own courses on TGD.